Comparing our framework to Andy Constan's "The Script"

Higher yields don't cause recessions; recessions cause lower yields.

In this installment of this series on Fed myth-making, we explore how interest rates and the economy affect each other. There are plenty of perspectives on this. One of those is Andy Constan’s (of Damped Spring Advisors) “The Script”.

As always, our goal here is to expose our thinking by comparing it against alternative frameworks.

In the first post, we discussed Jeff Snider’s views on the possibility of monetary deflation given the consistently pessimistic outlook priced into asset markets.

In the second post, we discussed Michael Howell’s views on the possibility of excess monetary inflation given central banks’ quick trigger for expanding liquidity.

In the third post, we discussed Lyn Alden’s views on the effects of QE in terms of raising nominal economic activity, which we don’t believe exist.

All of these frameworks are examples of Fed myth-making: they insert the Fed into the equation in ways in which the Fed can’t actually influence. That’s why the myth-making is necessary, because if executed well, the belief in Fed influence gives the Fed that influence.

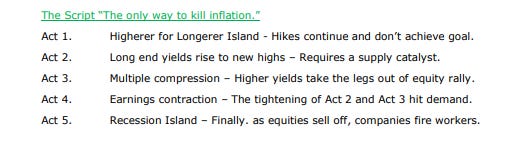

The Script describes Andy’s view of the order of linkages between the Fed’s interest rate hikes and the ultimate endpoint, a recession.

We think that The Script is another example of the Fed’s myth-making.

The core controversy here is: How do you square “higher yields cause recessions” with “higher yields reflect a stronger economy”? The Script presumes that both can be true.

Our view is that high interest rates only reflect a strong economy. They don’t cause conditions that would be consistent with lower interest rates. They cannot cause a weaker economy.

Below we work through the mechanics behind the noise in those charts, starting with describing The Script and how it characterizes the interplay between rates and the economy.

Outlining The Script: “Higher yields lead to a hard landing”

Below are the steps in this process for reference.

To add a bit more color to this, the process he’s describing is something like:

Fed hikes rates, flattening and eventually inverting the Treasury yield curve.

Long-term Treasuries start to look unattractive versus cash/T-Bills, so people sell duration which causes long-term yields to rise.

Higher long-term Treasury yields make Treasuries look attractive relative to stocks, causing equity valuations to fall as people move from stocks to bonds.

The higher cost of capital and interest burden for the private sector reduces additional borrowing and free cash flow, reducing earnings.

Businesses respond to the earnings contraction by laying off workers.

We at TMF take issue with all of these linkages. At a basic level, we know the Fed cannot cause a recession by changing long term rates, only shock short rates to a Taylor Rule like excess which quickly returns to a neutral rate. This Fed is raising rates to only neutral and then through long drawn out gradualism which makes even that rate change neutered if not add to NGDP growth. Instead we see risk-free rates as determined specifically by the forward expectations for nominal growth in the economy. And these risk-free rates can and do disconnect from Fed-administered rates when the Fed’s rates are out of sync with economic conditions.

In a recession, both that risk-free rate and nominal growth fall together.

Empirically, the steps described in The Script do not occur, and/or result in a recession. One cannot find an example when this was so. The Volcker rate rise was only addressing Fed Funds level. This is the only time one can find where a Fed Funds rate effected the economy, all other times since Fed Funds followed, not led.

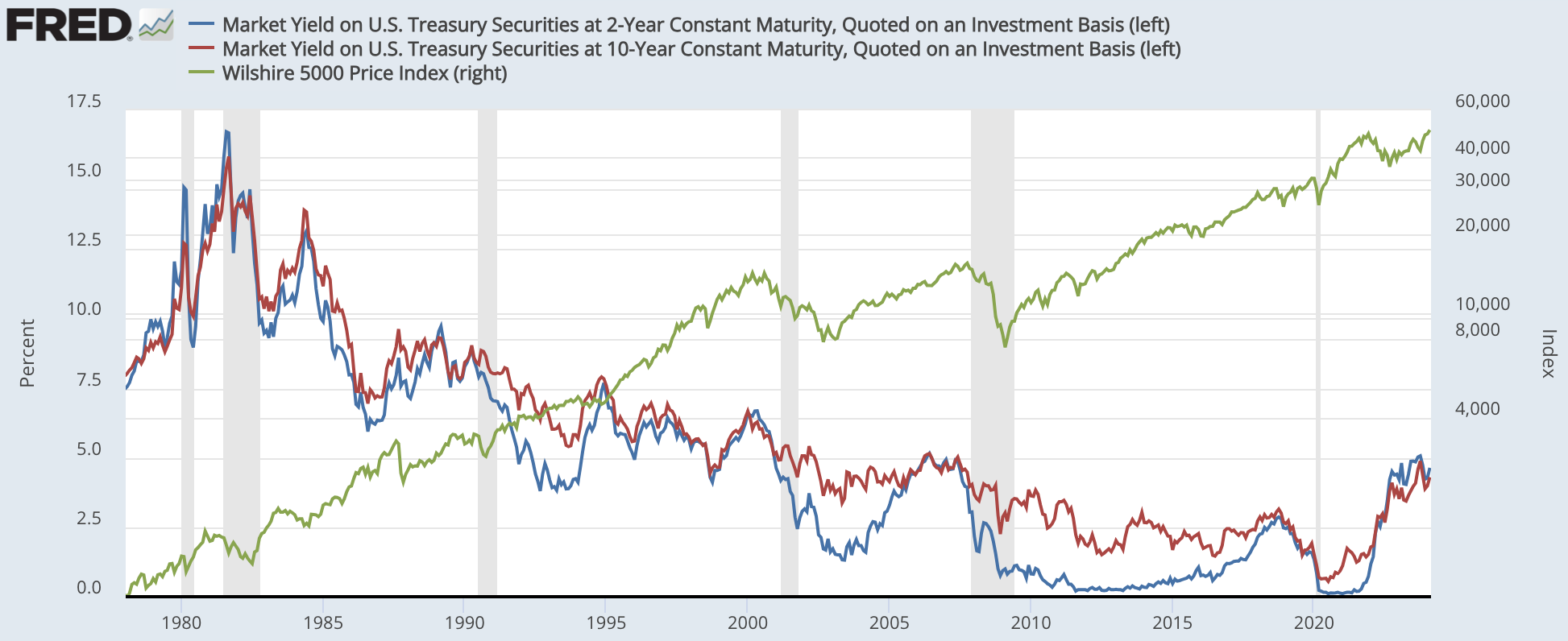

First, equities almost never decline during periods of rising rates. In the periods 1986-88, 1998-99, 2003-05, 2016-19, and 2023-, interest rates experienced significant increases, and equities rose without issue. This is consistent with our framework that the underlying driver of a sustainable increase in interest rates, an increase in NGDP expectations, is also what drives an increase in equity prices. When equities ultimately fell shortly after each of these periods, interest rates had already been falling.

Second, there is little to no relationship between equity PE ratios and long-term Treasury rates, for similar reasons: equity multiples are driven by a desire to hold risky assets, and typically that desire is high in periods of high interest rates. The high interest rates reflect a perceived lack of value in safe assets like Treasuries.

Third, “bear steepenings” in the Treasury yield curve are a frequent and do not impact the economy nor equity levels .

To the extent that the Treasury yield curve reflects the risk free rate, a rise in long-term rates absent rate hikes by the Fed is a bullish indicator for the economy, driven by rising nominal growth expectations.

In periods like today, where the Treasury yield curve is disconnected from the true risk free rate (something we have discussed at length), the idea of a bear steepening is at best completely irrelevant to an understanding of economic conditions.

Finally, it is well known that empirically, periods of high interest rates are associated with periods of high nominal growth, not periods of low nominal growth. This is the core thesis of Richard Werner’s paper on monetary policy, in which he argues the causality runs from economic conditions to rates, not rates to conditions, and that this relationship is positive, not negative.

Of course, the Fed (and any analysis that dismisses this empirical reality) has a convenient means to explain away these findings: long and variable lags.

Long and variable lags means the Fed can take credit for any recession or any expansion, and associate that economic outcome with its interest rate policy from any period prior. This is the cycle of unfalsifiable monetary policymaking:

The Fed is a necessary component for The Script, and The Script is necessary to legitimize the Fed.

If we at TMF came up with our own The Script, it would be very different than Andy’s, but much simpler, and one that fits the empirical reality discussed above:

Together, rates rise, earnings expand, equity prices rise, employment rises, home prices rise.

???

Together, rates fall, earnings fall, equity prices fall, employment falls, home prices fall.

The Fed is not a significant piece of Step 2. But with a strong enough belief system in the Fed and the Fed’s myth-making, the Fed can create the appearance of inserting itself into Step 2, manipulating sentiment and expectations enough to take credit for the unpredictable and unexpected transition to Step 3. We see Andy’s The Script as one of those myth-making exercises.

With a strong enough belief system in place, the Fed can claim credit for a recession through a self-fulfilling prophecy. The Fed attempted this with all its might in 2022-23, producing some clear changes in sentiment, but importantly, no clear changes in the monetary flows.

Those large changes in sentiment failed to produce a recession, because ultimately, it’s macro financial flows that dictate economic outcomes, not sentiment, psychology, or expectations. As a result, the decline in sentiment that began in early 2022 was a fade for the history books. Those that bought the sentiment ended up on the wrong side, because they believed in the potency of the Fed.

The Fed has convinced many that it was behind each of the last half dozen recessions, which led folks to conclude that the current Fed “tightening cycle” would produce a similar outcome.

As long as that narrative continues to fail to materialize, we see the Fed as in an existential crisis regarding its credibility and relevance. That crisis began in the early 2010s with the Fed’s inability to achieve 2% inflation, and every macro analysis that continued to invest faith in the Fed’s ability to “get what it wants” (the bond vigilantes pre-Covid, the recessionistas post-Covid) has consistently been on the wrong side of history since.

The Fed’s primary transmission mechanism is sentiment, not lending, stock prices, or wealth effects.

Central to Andy’s The Script is the idea that the Fed, in a complex system like the economy, can pull specific levers to achieve specific outcomes, and ultimately produce a recession in a fairly orderly fashion starting from that particular lever.

We see that notion as pure Fed myth-making, unsupported by the empirical reality or logical macro linkages.

Instead, it’s psychological manipulation and sentiment that is the Fed’s primary lever. And the more powerful this lever, the less the mechanical linkages matter, which is why the Fed is so dependent on maintaining a sophisticated media and expectations-management system that can influence sentiment to a large degree.

This is not conspiratorial, it is there in the transcripts. The Fed, over the last 40 years, has engaged in a deliberate campaign to recharacterize high interest rates as “policy tightness” rather than “economic strength”, and low interest rates as “policy easing” rather than “economic weakness”.

Volcker identified this conundrum soon after being made Fed Chair.

And so began the development of Fed myth-making as a policy lever:

Monetary policy is indeed a “psych-op”, and frameworks like The Script are instrumental to upholding that psych-op, giving the Fed the appearance of managing the economy through macro linkages, a power the Fed simply doesn’t have, especially in a world of fiscal dominance.

The Minsky framework as a better explanation of recessions.

Here is the issue with “high interest rates cause recessions”. It forgets that market prices simply reflect outcomes, they don’t change outcomes.

Take the market for sneakers as an example. If the price of a particular pair is going for $1000, the obvious interpretation of that price is that that shoe market is very strong. You might think it’s a bad time to buy those shoes, but ultimately the seller doesn’t care, because someone thinks it’s a good price to buy shoes at if the market is able to print that price.

Interest rates work the same way. If interest rates are high, it simply must mean someone thinks they’re getting a good deal by borrowing at that rate.

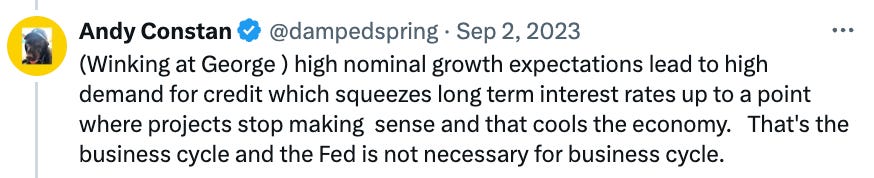

The below tweet, on this point, illustrates where I think Andy (and many others) misunderstand our framework regarding the ineffectiveness of the Fed.

Our argument is very much NOT that the Fed is not necessary for the business cycle. We think having a Fed is very important. We just don’t think that the Fed as it currently operates is able to serve that function.

Andy’s idea in that tweet that high growth leads to high rates which then work against the high growth is frankly bizarre. The implication is that high prices on credit (or shoes) ultimately produce low prices on credit (or shoes). This goes completely against the basic idea that market prices are reflections of market conditions.

The point is that if high nominal growth expectations are high, then the economy can and will borrow at high rates. If rates go even higher, it must be because nominal growth expectations rose even more. If they didn’t, then rates wouldn’t have gone higher, at least for very long.

The market price is the market price. Prices cannot produce conditions that would be consistent with different prices.

We have done work in the past de-linking Treasury yields from economic conditions and nominal growth expectations. The economy is built on a risk-free rate, and that doesn’t have to be the Treasury yield.

So what causes recessions? The turning point is Step 2 in the TMF version of The Script:

Together, rates rise, earnings expand, equity prices rise, employment rises, home prices rise.

???

Together, rates fall, earnings fall, equity prices fall, employment falls, home prices fall.

Ultimately, what goes in Step 2 is the Ponzi phase of a classic 3-stage Minsky framework, beginning with the hedge phase where risk-taking is done by the safest borrowers, then moving to the speculative phase and ultimately the Ponzi phase, which requires perpetual asset price appreciation to cover interest burdens. We are entering the part of that dynamic where the private sector is able and willing to take the reins in the event that this unprecedented fiscal impulse begins to pare down.

The Fed has little to do with when, or how, that Minsky moment turning point occurs. The Fed is only there to influence sentiment and expectations, and to serve as a hero for some and a villain for others. At TMF we recognize that the Fed doesn’t serve either of these functions, and by shedding the Fed, we can focus on the flows that matter and be positioned for when other market participants inevitably shed the Fed.

Bob Elliot makes a better case for the script Act 4 if I understand him. The current savings rate is depressed because it does not need to be higher given asset price appreciation. When multiples compress, asset prices will fall and savings will have to increase and reduce consumption. It is this reduction in consumption that reduces earnings and brings recession in a feedback loop.

Any thoughts?

Succinctly, the way I understand the script, it is that a rise in yields in long maturities it is a necessary condition to tight economic conditions, and render restrictive monetary policy effective, as it increases borrowing costs in the long end. Here, the Treasury, more than the Fed, is the main character. As conditions tight, equity multiples compress and earnings margins decline, ultimately leading to deleveraging, to lay offs, and recession. So, there is a sequence in the relation between high yields and equity falling, they are not coincident. Indeed, although not explicitly, it seems to me implied in Constan's piece that equity falling would be coincident with yields falling again.