It is important to have a understanding and then opinion on Neo Wicksell

It is important to have a understanding and then opinion on Neo Wicksell

To not understand Neo Wicksell means exposure to being baffled by major changes in the market - blindsided and likely ruin.

Those frustrated with my citing Neo Wicksell/Woodford, yet are too lazy to take the time to dig up stuff as to what it is - here as a great summation. Note when this was written - 2009 - when most Central Bankers were still optimistic that Neo Wicksell would "work". It did not “work” and the thesis has become an albatross around the Federal Reserve neck with likely Powell’s major concern is figure out how to dump Neo Wicksell and return to a Taylor Rule like policy.

While was mentioned by Bernanke and others as early as 2002, the idea of Neo Wicksell appeared as the Fed’s monetary policy when Michael Woodford presented Jackson Hole 2012 is a long read, there are many summations of this that is more approachable. here is John Cochrane 2012 critique.

Cochrane perceived Woodford speech in terms of “NGDP” targeting which in macro economic thesis of Irving Fisher, the risk free rate is one and the same as the annual change, or rate, of Nominal Gross National Product. It was not apparent that Bernanke followed by Yellen and Williams would see NGDP targeting not in Fisher ideas of the “Fisher Effect”.

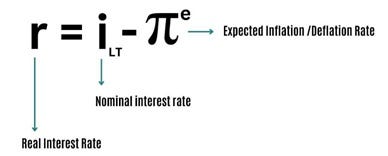

Where “i” can be changed such that monetary policy ends in reaching dual mandates goals of inflation and or full employment. - with either r being lowered to raise employment or “i” raised to to lower inflation. This is as Wicksell is based in the main of there being a “natural” long term “i” that is steady such that if the Fed raises “i” above this natural rate and cumulative drain or tightening results and if “i” can be lower than the Wicksell natural rate, then a cumulative add or ease results. The most important aspect of the Wicksell natural rate is the cumulative can be developed in a control manner such that the system stability continues, while the monetary policy prior to this Neo Wicksell depending on a “natural rate” targeted not the price level in inflation, but that “i” must be raised quickly and even in a shock so to be immediately a tighten or ease with the target being the immediate response in the inflation and employment. Fisher tenets pre-Neo Wicksell lay out, perversely, that the flow of funds generated by higher nominal interest rates will raise inflation and even real rates (real growth) if consistent and the economy understands that the higher Fed Funds rates will be quasi permanent.

And this is what has happened. The gradual raise of Fed Funds from 0% in February 2022 to 5 3/8% by August of 2024 made gradually in discreet steady raises well telegraphed ahead and with no reaction function or rule to provide a sense that the nominal levels of NGDP would stay high - the opposite goal as to what Powell announced 2022 to date.

Neo Wicksell given that there is no cumulative but an obvious Fisherian boast in NGDP (thereby inflation and real growth) as long as it is felt that the Fed Funds level will be unchanged and if changed will be in a gradual fashion.

In short, the rise in Fed Funds to 5 3/8% was stimulative, not a trightening, and remains so now.

The early supportive discussion of the new Neo Wicksell monetary policy was supportive as there was no idea that it would not work. And here is Paul Krugman supportive NY Times spiel; on Woodford Jackson Hole 2012.

And here is the Woodford paper - it is long but historically important which sought to explain how Fed can conduct monetary policy without a reaction function as per Neo Wicksell ideas given that Fed Funds were at 0% and could not be lowered into negative rates.

The key issue of Neo Wicksell implemented as Woodford use of forward guidance with no reaction function given ZIRP, is it sums up nicely that the central bank can either manage to the "price level" using Woodford or manage to the inflation and output gap. The current Fed feels should always manage to the price level and even more so, to the expected price level, expectations, and not worry about spot or here and now price level. Neo Wicksell feels inflation not at the goal is transitory if the Fed is maintaining a Fed Funds that ends with "natural rate". The likely most important results of Neo Wicksell implemented by Woodford was it allowed the Fed to conduct monetary policy and not disturbing the stability of the system, by not raising volatility. So when Fed Funds rose above 0%, there still was no reaction function and the Woodford methods which were for the times of ZIRP were maintained permanently. The Taylor Rule and the Fisher ideas behind Taylor were dismissed.

Now, under Neo Wicksell implemented by Woodford, the central bank waits for the return of inflation to the goal rate given the long term dedication of the Fed to the "natural rate". But the use of Woodford monetary policy, which is just talk and signals relaying on communicating only the Fed’s intent in the forward space, has no current reality, no reaction function.

The last 10 years have proven Neo Wicksell does not work, especially with only Woodford policy tools. This monetary policy tactic did not work to raise inflation from 2010 to 2019 to goal 2% no matter how many years at ZIRP or ZLB, and hasn’t worked to drop inflation post Covid.

The elimination of a reaction function to respond to an output gap nor an inflation to goal inflation gap - means that there is no monetary policy at all now given that Neo Wicksell ideals do not work.

If the Fed continues to carry on using Neo Wicksell with just Woodford tools, when an emergency occurs in the future, a Bagehot liquidity crisis occurs or a chronic "pushing on a string" policy failure then things get very serious as sooner or later the markets realize there is no emergency response available to a monetary crisis given the Neo Wicksell a la Woodford strait jacket.

Until such an emergency and the likely outcome shortly to the markets we will end with what is first a pleasant exuberant environment in a rally but once the rally becomes mania given the lack of effective Fed ability to drain and given the current stalemate in Congress, this mania will become a crash a severe crash. For with this crash, this Minsky Moment, there is no rescue or even basic Bagehot emergency liquidity provision to be expected from this Fed.

All the above will end, on the present course and basic ignorance of the market to the failure of Neo Wicksell/Woodford, with the ruin of most reading this now as while the mania will be at first welcomed, the attached doubling in volatility will perplex. Unless one understands this failure in current monetary policy the ending of the exuberance, or mania, will not be noted given the Fed will likely carry on with forward guidance and no here and now monetary policy. The crash will likely result in a serious depression, worse than the Covid experience as we go through wrenching changes as the nation “rescues” the Fed and returns the Fed to being, once again, a monetary agency operating in the here and now.

This is a note from Charles Gave I received before ordering his book on Wicksell:

"I wrote a book in Gavekal on Wicksell, a few years ago. I would not change a line. Maybe you could ask for a copy...

More seriously

For me, the market rate is equal to the BAA YIELD (MOODY'S seasoned industrials, data since 1920) from which I subtract the average inflation of the previous ten years.

The natural rate is the structural growth rate of corporate earnings , which I assume to be equal to the structural growth rate of the GDP. since, over the long term the ratio of corporate earnings to GDP tends to be flat.

If the central bank maintains short rates on the structural growth rate of the GDP, then the only ones that can borrow are those that have a ROIC > than the growth rate of the economy and most of the savings will go into the formation of NEW capital . And this debt will be eventually reimbursed, and we will have no inflation with money supply not growing

This is what we had in the US from 1982 to 2005, and it was called the great moderation

Since then, we have had short rates well below the growth rate of GDP, led the market rate to be well below the natural

It paid to borrow to buy existing assets . No new assets were created , productivity went down, the rich got richer, the poor got poorer, the budget deficits exploded and it led to the lost decade (s).

These policies lead to a massive increase in debt not accompanied by an increase in the capital base and no decrease in the money supply. These policies always lead to stagflation eventually

To use Musk's idea of the monetary system being the operating system of capitalism, when the market rate is maintained too low, it ALWAYS leads to the players in the monetary system to create too many false assets that they use to buy the entrepreneurs on the cheap

This leads to a massive transfer of wealth to these fellows from the hard working part of the population to those working in the monetary system and always ends in massive financial and social disorders.

I hope this helps

Charles Gave"